Biden’s plan to cancel scholar debt can apply to billions of {dollars} in investor-owned loans, however there’s a hitch

[ad_1]

The Biden administration’s plan to cancel as much as $20,000 in scholar debt isn’t restricted to debtors looking for reduction on loans the federal government already owns.

Roughly $110 billion in older “privately” held scholar loans created underneath the now defunct Federal Family Education Loan Program (FFEL) additionally might qualify, even by they aren’t instantly eligible for debt reduction underneath President Biden’s plan, an individual with direct information of the matter instructed MarketWatch.

So long as they meet the earnings standards for the debt reduction plan, borrowers with FFEL loans held outdoors of the federal government’s attain, together with these packaged years in the past into bond offers, could be consolidated into a brand new federal “direct loan” to qualify for cancellation, in accordance with the Division.

If debtors with these loans take the federal government up on its provide to consolidate to obtain the debt reduction, it additionally might imply an surprising deluge of funds to bonds that profit traders.

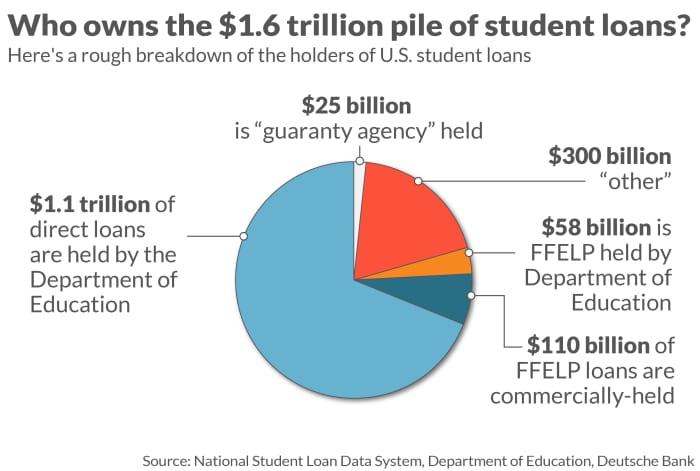

Who owns scholar loans

Like within the mortgage market, the U.S. authorities for many years has been the dominant participant in financing scholar loans.

With the Training Division’s roughly $1.1 trillion stake, the federal authorities owns all the pieces however a tiny slice (see chart) of the overall $1.6 trillion scholar mortgage pie.

MarketWatch illustration of how owns the $1.6 trillion pile of scholar loans

With the federal government’s outsized footprint, Biden’s debt reduction plan can attain most debtors incomes $125,000 or much less , however not all of them.

Earlier than 2010, banks and different personal lenders have been busy packaging billions value of government-backed FFEL scholar loans every year into asset-backed securities (ABS), or bond offers that promise to pay holders principal and curiosity funds over a sure time frame.

Deutsche Financial institution analysts estimated that issuance of FFEL asset-backed bonds averaged $6 billion yearly from 2018-2021, with an excellent tally as of the second quarter of about $110 billion.

“We’d count on a wave of prepayments,” stated Kayvan Darouian’s analysis staff at Deutsche Financial institution in a weekly shopper notice printed in August, notably if extra debtors obtain debt forgiveness underneath the Biden plan by consolidation.

Biden’s goal is to forgive as much as $10,000 for every eligible borrower making lower than $125,000 a 12 months, or $250,000 for a married couple. Eligible debtors who received Pell grants, or need-based monetary help, would see $20,000 canceled.

Whereas previous student-loan reduction applications have been troublesome for debtors to navigate and gradual to catch on, the prospect of sweeping debt cancellation might impress households.

FFEL ended during the Obama administration and was changed with direct authorities loans, regardless that most of the outdated loans in bond offers are nonetheless as a consequence of be repaid by debtors.

Learn: Biden’s $10,000 student-loan-debt relief plan could mean 15 million borrowers owe nothing

Do you have to consolidate?

The Client Monetary Safety Bureau, a shopper watchdog, in February updated its guide for debtors trying to consolidate scholar loans.

Since many college students take out new loans for every year of examine, consolidation right into a federal direct mortgage can mix a number of older loans into one mortgage. Consolidation doesn’t decrease a borrower’s rate of interest — the speed on the brand new mortgage is a weighted common of the loans that have been consolidated. However consolidating FFEL loans right into a direct mortgage provides different advantages, comparable to making the loan eligible for sure applications, together with a debt forgiveness initiative for public servants. For debtors with commercially held FFEL loans, consolidating can even make them eligible for the Biden administration’s broader debt reduction plan.

“For probably the most half, it’s an ideal alternative for debtors,” stated Persis Yu, coverage director and managing counsel on the Pupil Borrower Safety Middle, in a name with MarketWatch.

Nonetheless, there may very well be a couple of potential drawbacks, Yu stated, together with that excellent curiosity can be wrapped into the stability of the brand new direct mortgage, offsetting the scale of any debt cancellation. Additionally, any unresolved points with a previous lender, comparable to disputes over previous funds, can be waived underneath the brand new mortgage.

Lastly, debtors due for debt cancellation underneath the Corinthian College settlement, or from other for-profit colleges that the Biden administration stated misled college students would possibly wish to anticipate that reduction to be finalized earlier than consolidating, Yu stated.

Of notice, the Biden plan doesn’t embody decrease scholar mortgage charges. Personal lenders and plenty of refinancing startups like SoFi Applied sciences Inc.,

SOFI,

and Earnest started refinancing scholar loans roughly a decade in the past at decrease charges.

These loans can’t be consolidated into a brand new authorities direct mortgage. Nonetheless, over the subsequent couple of months, the Training Division will seek the advice of with personal lenders to contemplate offering reduction that features these loans, the individual stated.

Past debt cancellation, eligible debtors additionally would possibly wish to think about the federal government’s consolidation choice as a possible cost-saving measure if considered one of their scholar loans has a variable price (all federal scholar loans taken out by debtors on or after July 1, 2006 have a fixed rate of interest). The Federal Reserve plans to proceed elevating its benchmark rate to about 4% this year from its present 2.25%-2.5% vary to combat excessive inflation.

Price hikes make variable-rate debt costlier for debtors and might result in a better borrower defaults, which was a key catalyst some 15 years in the past of the subprime mortgage disaster.

Lenders ‘are going to monetize this’

Along with debt cancellation, Biden’s plan additionally bolsters current income-driven compensation plans for a lot of scholar loans, together with by capping month-to-month funds on undergraduate loans at 5% of a borrower’s discretionary earnings, as an alternative of the present 10% cap.

Whereas extra particulars are anticipated within the coming weeks, the White Home stated the trouble would give “households respiratory room” earlier than the pause on federal scholar mortgage funds put in place on the onset of the pandemic in 2020 is about to run out on the finish of December.

“We nonetheless don’t know what the specifics appear to be,” stated David Sacco, a former fixed-income dealer on Wall Avenue who now teaches finance on the College of New Haven. However he does suspect lenders have already got begun gearing up for shoppers to obtain some scholar debt reduction.

“The buyer finance corporations are going to be throughout this,” Sacco stated, including that whereas the Biden debt reduction targets solely lower-to-middle earnings households, many could have current mortgages, bank cards and different shopper debt, along with scholar loans.

“In some instances, entry to a $10,000 grant could be a significant down fee on a home,” he stated.

Considerations about larger charges

TMUBMUSD10Y,

and a possible U.S. recession have been weighing on equities after a short summer season rally. The Dow Jones Industrial Common

DJIA,

S&P 500 index

SPX,

and Nasdaq Composite Index

COMP,

have been all decrease Tuesday after Labor Day.

Source link