D’you recognize one of the best time to interview a C-suite government at an enormous music firm? Once they’ve already introduced they’re leaving.

That means, they could be a little much less tight-lipped. Rather less fearful about retaining the peace. A bit of extra ‘mic drop’.

That definitely utilized to Warner Music Group CEO, Steve Cooper, talking on the Goldman Sachs Communacopia + Expertise Convention in San Francisco on Monday (September 12).

Cooper, in fact, confirmed earlier this year that he’s to exit Warner in both 2022 or 2023, and is at present working the key because it searches for his successor.

The exec was sometimes thought-about in his Q&A session with Goldman – however he additionally didn’t miss the chance to deal with plenty of business speaking factors head-on and with stunning candor.

‘We’ve lowered our dependency on superstars’

Maybe the music business’s most head-turning quote of summer time 2022 got here from BMG‘s CEO, Hartwig Masuch, commenting on his agency’s H1 2021 monetary outcomes.

“The extraordinary factor about our first half result’s that we grew income 25% with just about no hits,” said the German exec in August.

Masuch’s “no hits” remark comes amid an ever-more fragmenting music business panorama the place new-release chart smashes – as a lot as each firm wishes and advantages from them – are claiming a lowering share of the worldwide market.

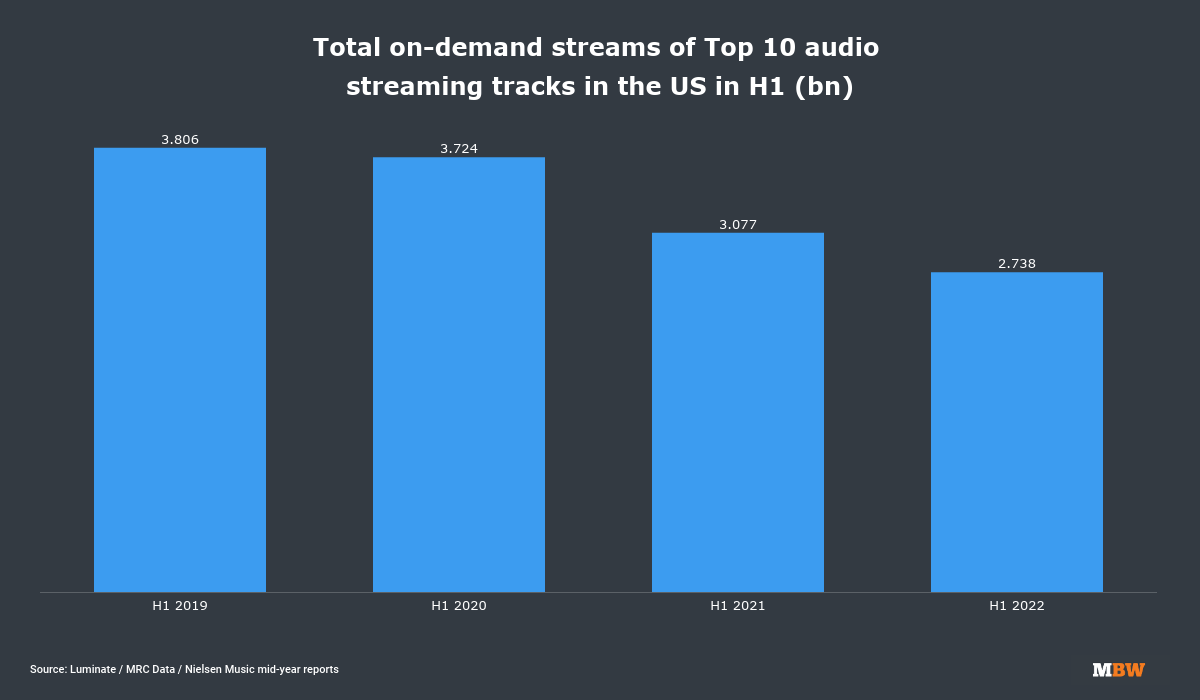

Take a look at the info: Based on MBW’s calculations of Luminate / MRC Data figures, the Prime 10 audio streaming tracks within the US in H1 2022 have been cumulatively performed over 1 billion instances lower than they have been in H1 2019 (2.74bn vs. 3.81bn)*.

In the meantime, celebrity artists are additionally inevitably taking on much less market share, as a result of dilution impact of streaming’s world subscriber development, plus the huge quantity of tracks launched every day.

Clearly sufficient, this altering image impacts the A&R and advertising and marketing technique of the key music corporations – specifically, how a lot finances allocation they think about established ‘celebrity’ artists versus spreading that finances amongst a wider pool of performers.

Talking at Communacopia on Monday, Cooper steered that Warner Music Group is now leaning in direction of the latter of those two choices, investing an “monumental quantity of A&R sources” throughout a much bigger variety of artists than it as soon as did – together with superstars and non-superstars.

This, he mentioned, constitutes a “portfolio” technique that on common leads to “mid to excessive teen [percentage] returns” for WMG.

Mentioned Cooper: “In working our portfolio, what we’ve completed over the past variety of years is cut back our [financial] dependency on superstars. [And] decreasing that dependency has allowed us to proceed to strengthen our strategy to A&R, which is long-term artist improvement.”

He added: “We attempt to discover artists in the beginning of their profession, in order that we will construct their profession with them, however [via] a set of economics that we imagine are cheap and rational, versus economics that we regularly observe in different offers that frankly we don’t perceive.”

“What we’ve completed over the past variety of years is cut back our dependency on superstars. [And] decreasing that dependency has allowed us to proceed to strengthen our strategy to A&R, which is long-term artist improvement.”

Steve Cooper

Cooper went on to reference Taylor Swift’s licensing and distribution cope with Universal Music Group / Republic Records, signed in 2018, below which Swift owns the recording copyrights to albums similar to Lover, Evermore, Folklore, and the ‘Taylor’s Model’ re-records of her earlier LPs.

Mentioned Cooper: “I don’t see [Warner’s] A&R [spend] rising explosively over the subsequent few years. I don’t learn about our rivals however we attempt to be very, very considerate and really centered and we don’t chase the warmth.

“By means of instance, when Taylor Swift moved from Big Machine to Common [in 2018], she acquired a monster verify and he or she acquired a really, very skinny distribution cost. We don’t do these offers; there’s not, from our perspective, the precise aspect of economics. We don’t chase massive names to get a little bit little bit of income and never make any cash.”

(Though it’s identified that Swift did certainly get a extremely favorable margin in her 2018 digital distribution cope with Republic/UMG within the US, it’s anticipated that Common’s margin in that deal will increase with bodily distribution, particularly in ex-US territories. Swift has additionally signed world publishing and merch offers with Common, that means UMG is taking a share of a extra holistic enterprise with the artist than simply information.)

At Communacopia, Steve Cooper additionally tackled the concept document firm offers with artists – particularly ‘scorching’ rising acts – are getting costlier.

Concerning the query of whether or not the financial worth of artist offers is usually rising for labels, he mentioned: “The reply is oftentimes sure. However [those deals] have gotten costlier as a result of we’re producing extra income. [Therefore] clearly we’re rising our backside line, and our artists take part in that development.

“As artists change into extra profitable and are extra essential in driving development with us, can we reevaluate their contracts and modify? Completely.”

Once more, it’s price looking on the numbers right here.

Based on Warner Music Group filings, WMG spent $326 million on recorded music A&R (artist and repertoire) prices within the second calendar quarter (fiscal Q3) of 2022. That was equal to27% of WMG’s recorded music income within the quarter.

For those who head again three years, pre-pandemic, to calendar Q2 2019, Warner spent $282 million on recorded music A&R (artist and repertoire prices).

That was equal to a considerably increased proportion (31%) of whole recorded music income. That 31% determine additionally carried for calendar Q2 in 2018.

This suits with Cooper’s declare that Warner is certainly spending considerably more cash on offers than it did in earlier years ($326m in calendar Q2 2022 vs. $282m in calendar Q2 2019).

But it surely additionally tells us that Warner is managing to cut back its A&R spend on recording artists as a proportion of its total revenues.

Credit score: Shutterstock/Diego Thomazini

‘The DSPs will in the end see the necessity to elevate costs’

Steve Cooper didn’t simply speak about A&R spending at Communicopia. One different massive subject of debate was the pricing of music streaming companies.

Some within the music business – Daniel Ekamongst them – argue that by not considerably elevating the standard particular person $9.99 / £9.99 / €9.99 month-to-month streaming subscription worth, the music business has insulated itself from the sort of subscription cancellations now hitting Netflix in a macro-economic downturn.

Others (together with Common Music Group investor Pershing Square) argue there’s nonetheless headroom to lift streaming costs, with out having a detrimental impact on subscriber churn.

Cooper’s view very a lot suits with the latter class – certainly, he desires to see “common” worth will increase rolling out at companies like Spotify.

At Communicopia, Cooper famous that ad-supported streaming platform payouts had seen an “affect from macro-economic influences” already in 2022, however famous that he was extra bullish on subscription, a enterprise he referred to as “very sticky”.

“the worth proposition [in music streaming] is unbelievable. That leads us to conclude that – notably with the stickiness and nearly non-existent churn – companies can simply elevate the month-to-month subscription by a fraction they usually can do it on a regularized foundation.”

Steve Cooper

Added Cooper: “[One] of the issues that we’re starting to see and hope to see on a regularized foundation is pricing will increase, along with simply the variety of individuals that can nonetheless be signing up for subscriptions [due to] additional penetration of smartphones.”

Cooper predicted that between “regular development” in streaming subscriber uptake, plus worth will increase, the probability of the document business sustaining double-digit YoY income development in subscription streaming is “extremely probably”.

He continued: “If you take a look at the worth proposition in music versus video, [it’s] unbelievable. That leads us to conclude that – notably with the stickiness and nearly non-existent churn – [music streaming] companies can simply elevate their month-to-month subscription by a fraction they usually can do it on a regularized foundation.

“We’re hopeful that given historic, present, and what I’m positive will likely be future discussions, the [music] DSPs will in the end see the necessity to elevate costs, elevate them repeatedly, and have a extra rational relationship between the worth and the worth that’s being delivered.”

He added: “Once I take a look at the DSP fashions, I’d conclude, fingers crossed, that these will increase will come sooner versus later.”

‘We lean in direction of the buyout mannequin’

One other controversial subject in B2B music business circles this yr has been the key document corporations’ offers with the likes of TikTok and Meta.

In recent times, these offers have been characterized as “buy-outs”, as a result of they usually see a service write a flat-fee verify to a rightsholder for a blanket license to make use of their music for 2 or extra years.

Some within the business have referred to as for the majors to unite of their insistence that these “buy-out” offers transfer extra in direction of the sort of revenue-share deal they’ve with YouTube, the place the Alphabet firm pays music rightsholders a proportion of each greenback generated by advertisements on their content material.

Meta moved nearer to this revenue-share mannequin earlier this yr, announcing deals with a number of music corporations – together with Common Music Group and Warner Music Group – that can see a sure proportion of promoting revenues shared with music rightsholders for sure kinds of UGC video on Facebook.

Steve Cooper stopped brief at naming TikTok particularly however did talk about the professionals and cons of those “buy-out” offers.

He mentioned at Communicopia that on the planet of “Internet 2.0” Warner primarily indicators two kinds of licensing offers: “regular subscription” with the likes of Spotify, Apple and YouTube, plus “what are basically buy-outs, extra carefully related to rising fashions on social platforms”.

“I believe we’ve acquired a pair extra turns on the buy-out [deals] earlier than we begin see to social, health and different socially-oriented platforms [build] sufficient of a historical past and have completed [enough] experimenting to [switch to a revenue-share licensing model].

Steve Cooper

Cooper then famous that WMG tends to “lean in direction of the buy-out mannequin” when it isn’t “positive in regards to the breadth and depth of how music will likely be adopted [on a service], and we’re undecided in regards to the development trajectory”.

In different phrases, it’s higher to financial institution some assured cash up entrance, than strike a revenue-share deal and watch a digital startup implode.

(With regards to TikTok, critics of the “buy-out” construction would level out that the Bytedance platform generated $4 billion final yr and is projected to generate $12 billion this yr, and that it has been downloaded over 2.6 billion times globally. That’s some “development trajectory”.)

Cooper added that, as rising platforms mature previous a sure level, “we and [the platform] will collectively shift from a buy-out to a use-case mannequin, the place we take part extra instantly within the development of music on these rising platforms”.

When requested to foretell when Warner may transfer from a buy-out mannequin to a revenue-share mannequin with sure key platforms, Cooper answered: “I believe we’ve acquired a pair extra turns on the buy-outs earlier than we see the social, health, and different socially-oriented platforms [build] sufficient of a historical past and have completed [enough] experimenting to actually make that flip.”

Cooper instructed the viewers that inside these buy-out offers, WMG will sometimes signal “a two-year contract” after which ups its worth (“a step operate”) at every renegotiation.Music Enterprise Worldwide