[ad_1]

MBW Reacts is a collection of brief remark items from the MBW staff. They’re our ‘fast take’ reactions – by way of a music biz lens – to main leisure information tales.

J.P. Morgan issued a glowing analysis word on UK-listed Hipgnosis Songs Fund on Monday (September 19).

“Given the long-term development potential of the asset class, and the upper high quality (in our view) portfolio relative to [Round Hill Music], we consider SONG affords compelling worth,” mentioned J.P Morgan, sustaining its ‘chubby’ ranking on HSF’s inventory.

J.P Morgan’s analysis word on Hipgnosis Songs Fund was a thundering vote of confidence in HSF’s enterprise, following a latest flurry of enterprise media scrutiny.

Particularly, a run of three related latest articles within the Financial Times on HSF every questioned points of Hipgnosis Songs Fund, together with:

- The very fact HSF hasn’t purchased a catalog up to now 12 months;

- The truth that it’s refusing to boost new funds;

- The affect of present macro-economic pressures on HSF’s worth, and its funds.

We’ll get to some necessary element behind all three of these shortly, and what J.P Morgan has to say about them.

However first issues first: Mentioned protection of HSF has led to some follow-up reporting, which in flip has led to the wonky conclusion in some quarters that ‘Hipgnosis has burned by way of its money’.

As a lot as that concept would possibly deliver glee to these with the knives out for Merck Mercuriadis’ firm, in actuality it’s flat-out flawed.

That’s as a result of Hipgnosis Songs Fund is not Hipgnosis; it’s one a part of a three-pronged Hipgnosis group.

That group has already spent roughly $300 million on music catalogs in 2022. Sources recommend that the present plan for this Hipgnosis group is to spend one other $300 million by the tip of the yr.

Briefly: Hipgnosis, the group, has entry to all capital it must do each conceivable artist/songwriter copyright acquisition in music.

It stays to be seen, nonetheless, how a rising price atmosphere would possibly complicate this image, with rates of interest now at their highest point since 2008 within the US and UK.

Table of Contents

Understanding Hipgnosis

To know the Hipgnosis group – and why it nonetheless has a possible pipeline of billions of {dollars} in its M&A arsenal – we first have to refresh our recollections of the three Hipgnosis-branded corporations:

- Hipgnosis Songs Fund (HSF): a UK-listed FTSE 250 firm that has acquired over $2 billion in catalogs thus far, which have collectively been given an independent valuation of $2.7 billion;

- Hipgnosis Songs Capital (HSC): a non-public fund, fully-funded by Blackstone, that has spent round $300 million buying copyrights in 2022 alone, from the likes of Justin Timberlake, Kenny Chesney and the Leonard Cohen property;

- Hipgnosis Tune Administration (HSM): a ‘track administration’ and Funding Administration firm that advises on the investments of HSF and HSC, and manages the belongings of each.

In essence, firm (iii) – Hipgnosis Tune Administration – chooses which catalogs to spend HSF’s and HSC’s cash on.

Over three years (2018-2021), HSM constructed up a portfolio for Hipgnosis Songs Fund of ≈65,000 copyrights from writers similar to Mark Ronson, Pink Scorching Chili Peppers, Neil Younger, Lindsey Buckingham, Difficult Stewart and lots of others.

Nevertheless, final summer time, HSM confirmed that its major supply of capital for offers had successfully switched to firm (iii): Hipgnosis Songs Capital.

The preliminary dedication to HSC from Blackstone was a billion dollars (a mixture of fairness and debt). Sources recommend this dedication remains to be anticipated to multiply over the following few years.

It’s this fund (HSC) that has spent $300 million on music rights in 2022 to date by way of HSM – and which is anticipated to spend someplace close to that once more within the the rest of the yr.

Rising rates of interest, nonetheless, are more likely to put a cap on the multiples any music firm is prepared to pay for copyright buyouts within the present atmosphere.

Except potential sellers are prepared to drop their desired a number of to this stage, we might even see one thing of a cool-down within the music M&An area within the months forward.

(There’s a flip-side to this example: Some artists and songwriters might certainly be prepared to promote at a decrease a number of than their friends achieved in recent times – as a result of as soon as they’ve cash within the financial institution, high-interest charges and a battered inventory market arguably create an funding market the place mentioned cash can rapidly acquire in worth.)

Why is Hipgnosis Tune Fund not elevating cash?

For informal observers of Hipgnosis Songs Fund (HSF) – which has spent over USD $2 billion on catalogs since being based in 2018 – the present halt in its spending exercise might come as a shock.

But for HSF traders, and people extra intently watching the corporate, it’s not precisely surprising.

Hipgnosis Songs Fund informed its shareholders when it raised $215 million final July that it was placing a cease on additional raises till Q2 2022 on the earliest.

The next month, in August 2021, HSF informed traders that it was “fully invested”, following acquisitions of a number of catalogs (utilizing that $215m) together with music by the Pink Scorching Chili Peppers and Christine McVie of Fleetwood Mac.

Q2 2022 has now been and gone, which implies HSF is free from its self-imposed moratorium on elevating cash. However market circumstances don’t seem like they did final summer time.

Particularly, with the twin shocks of a steep rise in inflation plus the warfare in Ukraine, public share costs throughout the board have been hit onerous.

Publicly traded music compares haven’t been proof against this pattern: Hipgnosis Songs Fund is down 20% YTD in 2022; Universal Music Group is down 27%; Reservoir is down 33%; Warner Music Group is down 42%; Spotify is down 50%; Believe is down 58%.

It’s due to this fact unlikely that corporations like these would select to boost new fairness (by way of share points) at present inventory costs as it could harm the holdings of present shareholders. In accordance, HSF has opted not to take action.

One other barrier to Hipgnosis elevating cash proper now: these rising rates of interest.

HSF at the moment has a debt stack of $600 million. The price of servicing that debt will increase with each rate of interest rise.

That being mentioned, HSF confirmed to shareholders this week that it has now secured a brand new debt refinancing package deal. J.P Morgan was impressed with this information, saying this refi is “anticipated to decrease [HSF’s] facility price and improve its measurement”.

As MBW defined in November, HSF – as long as it has the funds out there – can opt to acquire a 20% stake alongside HSC (by way of the latter’s billion-dollar-plus pot of Blackstone cash) in any catalog buyout proposed by HSM.

Why is Hipgnosis Songs Fund’s Professional-forma income declining?

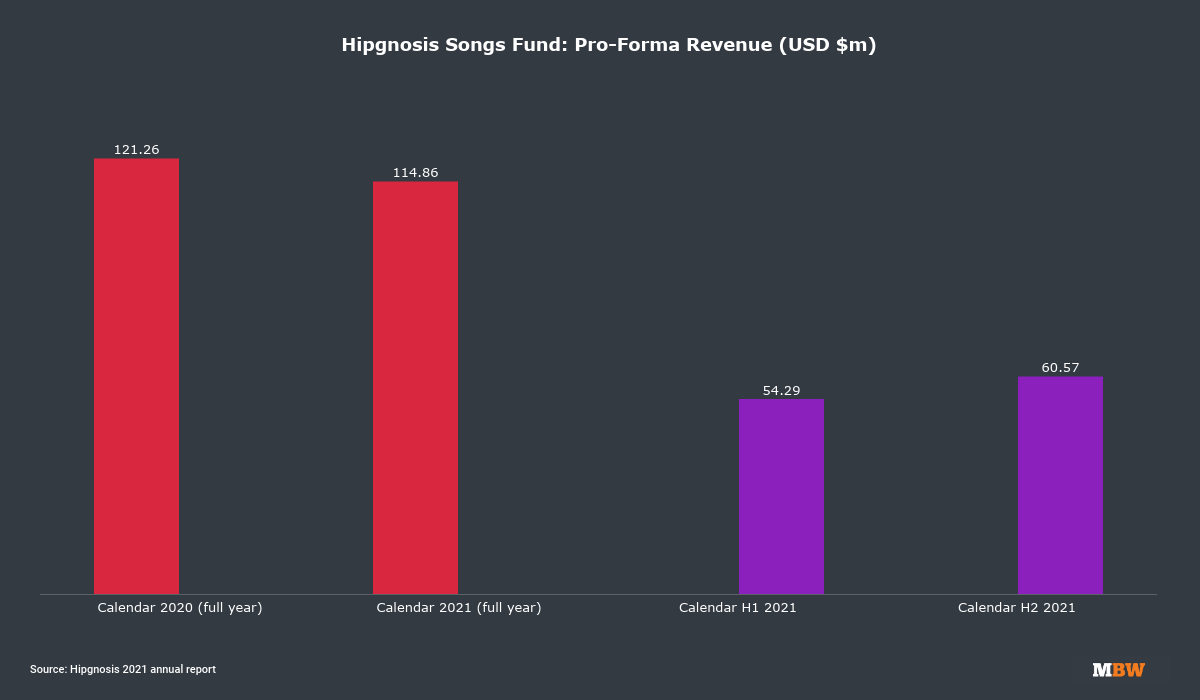

One main matter raised by financial media outlets in latest weeks: The ‘Professional-forma’ income (PFAR) of Hipgnosis Songs Fund declined YoY in HSF’s FY 2022 (to finish of March 2022).

On the floor of it, this definitely seems troubling: ‘Professional-forma’ income (PFAR), which HSF voluntarily publishes, exhibits the royalty income earned by catalogs in a calendar yr primarily based on royalty statements obtained, regardless of whether or not the songs have been owned by the corporate over the interval analyzed. It’s a ‘pure’ like-for-like reflection of how catalogs are performing.

You’d count on a certain quantity of decline every year in ‘Professional-forma’ income at an organization like Hipgnosis Songs Fund on account of newer catalogs; i.e. catalogs which might be nonetheless ‘leveling off’ from their industrial peak earlier than they hit a long-tail plateau.

In flip, you’d count on these declines to be offset by an increase in earnings from older catalogs which have already hit that plateau.

For instance, inside HSF’s catalog of songs, you’d count on Form Of You (launched in 2017) to nonetheless be on a robust decay curve, however you’d count on classics from Neil Younger, Lindsey Buckingham, Bon Jovi and so on. to be rising annual income as they trip streaming’s development.

So what went awry inside HSF’s ‘Professional-forma’ income in FY 2022? In a phrase: Covid.

Performing rights societies throughout the globe usually account to publishing rights-holders 12 to 18 months behind the second of consumption. Inside HSF’s numbers proper now, that lag is essential.

Should you return 12 to 18 months from the tip of HSF’s newest fiscal yr (March 2022), you land on the coronary heart of the best stage of adverse affect that COVID lockdowns had on all companies.

Thus, there’s a considerable quantity of efficiency revenues from world wide – music being performed in bars, eating places, retailers, nightclubs, and all the dwell performances by artists – that may have been there in ‘regular’ circumstances however should not mirrored in HSF’s numbers.

“We count on a really sturdy bounce again in [Hipgnosis songs Fund’s] efficiency earnings.”

J.P. Morgan

This Covid-driven income deficit is arguably extra pronounced for corporations like HSF than it’s for the main music corporations, as a result of HSF is solely within the catalog enterprise; it doesn’t have a streaming money bump from new frontline hits to offset the adverse affect from Covid lockdowns.

J.P. Morgan this week famous why it was unworried by the ‘Professional-forma’ decline in Hipgnosis Songs Fund’s numbers for FY 2022, stating: “We count on a really sturdy bounce again in [HSF’s] efficiency earnings (ex the efficiency factor of streaming, which is classed by SONG as ‘streaming’ however in actuality is a mix of mechanical and efficiency), which was late to indicate up within the PFAR numbers, but additionally late to get better given the lag vs UMG and WMG.”

The early indicators of that restoration have been really already there inside HSF’s FY 2022 numbers:

- For the complete calendar yr 2021, HSF’s PFAR was certainly down 5.3% YoY;

- However within the second half of 2021 alone (July- December), HSF’s PFAR was up (vs the primary half of 2021) by double digits (+11.6%, see under)

(How a lot HSF traders actually care in regards to the PFAR vs. the corporate’s potential to pay its anticipated dividends is one other matter. At its AGM this week, Hipgnosis confirmed it could pay its interim 2022 dividend in October on the anticipated worth, and reiterated it was heading in the right direction to pay its full-year dividend, additionally on the anticipated worth, in March 2023. J.P. Morgan appeared happy by this information.)

Hipgnosis Tune Administration x Blackstone

One other query mark raised by latest reporting factors particularly to Hipgnosis Tune Administration (HSM) and Blackstone’s stage of involvement within the firm.

Nearly a yr in the past, Hipgnosis introduced its partnership with Blackstone, with the funding big absolutely funding Hipgnosis Songs Capital (HSC), whereas making an undisclosed funding into Hipgnosis Tune Administration (HSM).

MBW has carried out some digging, and understands that Blackstone owns 51% of HSM, with Mercuriadis and his household proudly owning 35% and long-standing Hipgnosis allies, together with Nile Rodgers, proudly owning the rest. As CEO, Mercuriadis runs the corporate.

Critics of this mannequin would possibly recommend that Blackstone’s majority (51%) possession of HSM may give the personal, Blackstone-funded Hipgnosis fund (HSC) unfair desire throughout the Hipgnosis group (the general public fund, HSF, is owned by many different exterior traders, together with the Church of England).

On a extra optimistic word, Hipgnosis’ strategic significance to Blackstone is unquestionably highlighted by advantage of the controlling stake that Blackstone determined to amass in HSM. (Plus, as talked about, HSF – as long as it might probably discover the cash – has blanket co-investment rights on every part HSM sources and seeks to amass.)

Whatever the Hipgnosis group construction, the importance of getting Blackstone as a dedicated investor in music rights shouldn’t be underestimated.

Blackstone had $881 billion in complete belongings beneath administration (AUM) in FY 2021, and can doubtless have someplace near a trillion {dollars} in complete belongings beneath administration by the tip of FY 2022.

As talked about earlier: Hipgnosis’ entry to piles upon piles of personal capital is just not in query.

A controversial low cost price – and a few very well timed headwinds

One other side picked up in latest reporting from the Monetary Occasions and others was the best way by which Hipgnosis Songs Fund (the UK-listed firm) is independently valued each six months.

To worth HSF, the corporate turns to a gaggle of music trade consultants inside Citrin Cooperman. This group beforehand operated as Massarsky Consulting earlier than being acquired by Citrin Cooperman earlier this yr.

Questions have been raised over Citrin Cooperman’s insistence that an 8.5% ‘low cost price’ stays adequate for music valuations regardless of quickly rising rates of interest within the US, UK and elsewhere.

To maintain it easy: If this low cost price was to be elevated by Citrin, it could decrease the worth of Hipgnosis Songs Fund on a NAV (Web Asset Worth) foundation.

J.P Morgan, although, says it continues to be happy with the 8.5% low cost price, and sees no want for adjustment.

The funding firm mentioned in its analysis word this week: “We really assume an 8.5% low cost price regarded massively conservative earlier within the yr till US lengthy charges began to rise… now we consider it seems cheap given the still-big threat premium and decrease beta of music because it has develop into a subscription-based utility annuity stream.”

In fact, with heavy inflation, a dwindling inventory market, and the Fed ratcheting up these rates of interest, corporations like Hipgnosis Songs Fund are having to sort out some substantial macroeconomic headwinds immediately.

But J.P Morgan notes that there’s additionally a widespread variety of ‘tail-winds’ serving to enhance the longer term prospects for HSF (and the broader Hipgnosis group).

The J.P Morgan analysis word this week, penned by Christopher Brown and Adam Kelly, famous the latest ‘CRB III’ decision, which upheld higher mechanical charges for songwriters and publishers within the US for the years 2018-2022.

Consequently, the likes of Spotify, Amazon Music and different streamers are having to pay one-time cash to publishers with the intention to fulfill retrospective charges on this interval: Warner Music Group, for instance, recently reported a $17 million windfall from the CRB III catch-up course of in calendar Q2.

J.P Morgan additionally likes the look of the recently-inked ‘CRB IV’ agreement between publishers and streaming companies within the States, which might set the mechanical headline price paid to pubcos at 15.35% of every streamer’s US income.

“We’re optimistic about income [at Hipgnosis Songs Fund] over the approaching yr, with [many] optimistic drivers.”

J.P. Morgan

If ratified by the Copyright Royalty Board judges within the US, this may barely improve the mechanical price paid to publishers from 2023-2027 within the US on account of CRB III.

What’s extra, the historic power of the US greenback vs. the British pound works in Hipgnosis Songs Fund’s favor with regards to paying its UK dividends (the vast majority of the corporate’s revenues are generated within the US).

Mixed with HSF’s debt refinancing, this run of stories has put J.P Morgan in a buoyant temper.

The funding agency’s word this week mentioned it was “optimistic about income [at HSF] over the approaching yr, with [many] optimistic drivers”, together with an anticipated improve in streaming subscription income and potential worth rises on companies like Spotify.

J.P Morgan can also be eager on the affect that the Mechanical Licensing Collective (MLC) is having within the States, forecasting that it “ought to result in greater payouts from US streaming [to HSF], with extra environment friendly, commission-free collections from DSPs”.

Moreover, J.P Morgan means that HSF will profit from some “first time contributions to come back from rising digital platforms, not hitherto in SONG’s proforma annual income”.Music Enterprise Worldwide

Source link