[ad_1]

Credit score strains are a profitable product. U.S. customers alone pay $120 billion in bank card curiosity and costs yearly, in keeping with the Client Monetary Safety Bureau. Given the income alternative, it’s no shock that there’s enduring curiosity from each startups and established firms in delivering credit-based merchandise. However challenges stand in the way in which, together with — however not restricted to — complying with native legal guidelines and rules and modeling credit score danger.

Enter Noble, a putative answer within the type of a platform that enables companies to construct credit-based merchandise like bank cards and purchase now, pay later companies with no-code instruments. Based by WeWork veterans, Noble permits shoppers to attach information sources to create customized credit score choices, offering a rules-based engine to edit and launch credit score fashions.

Noble as we speak emerged from stealth and introduced the shut of a $15 million Sequence A spherical led by Perception Companions with participation from Cross River Digital Ventures, Plug & Play Ventures, Y Combinator, Flexport Fund, TLV Companions, Operator Companions, Verissimo Ventures, Interaction Ventures and the George Kaiser Household Basis. The brand new money brings the corporate’s whole raised to $18 million, which CEO Tomer Biger tells TechCrunch will go towards opening a brand new workplace and increasing Noble’s portfolio to help extra use instances.

Connecting information sources in Noble’s admin dashboard. Picture Credit: Noble

Biger and Noble’s CTO, Moran Mishan, labored collectively at WeWork on constructing underwriting infrastructure to assist display screen and assess the creditworthiness of tenants. Previous to WeWork, Biger was the product supervisor chargeable for business-to-business (B2B) lender Behalf’s underwriting infrastructure, whereas Mishan was a software program engineer at Woo.io, a job candidate sourcing platform.

“From these firsthand experiences, [we] noticed how difficult it’s for firms to construct underwriting infrastructure and launch new credit-based merchandise, Noble goals to vary that,” Biger informed TechCrunch in an e-mail interview. “[We allow] firms to launch extra merchandise that their end-customers need — entry to credit score.”

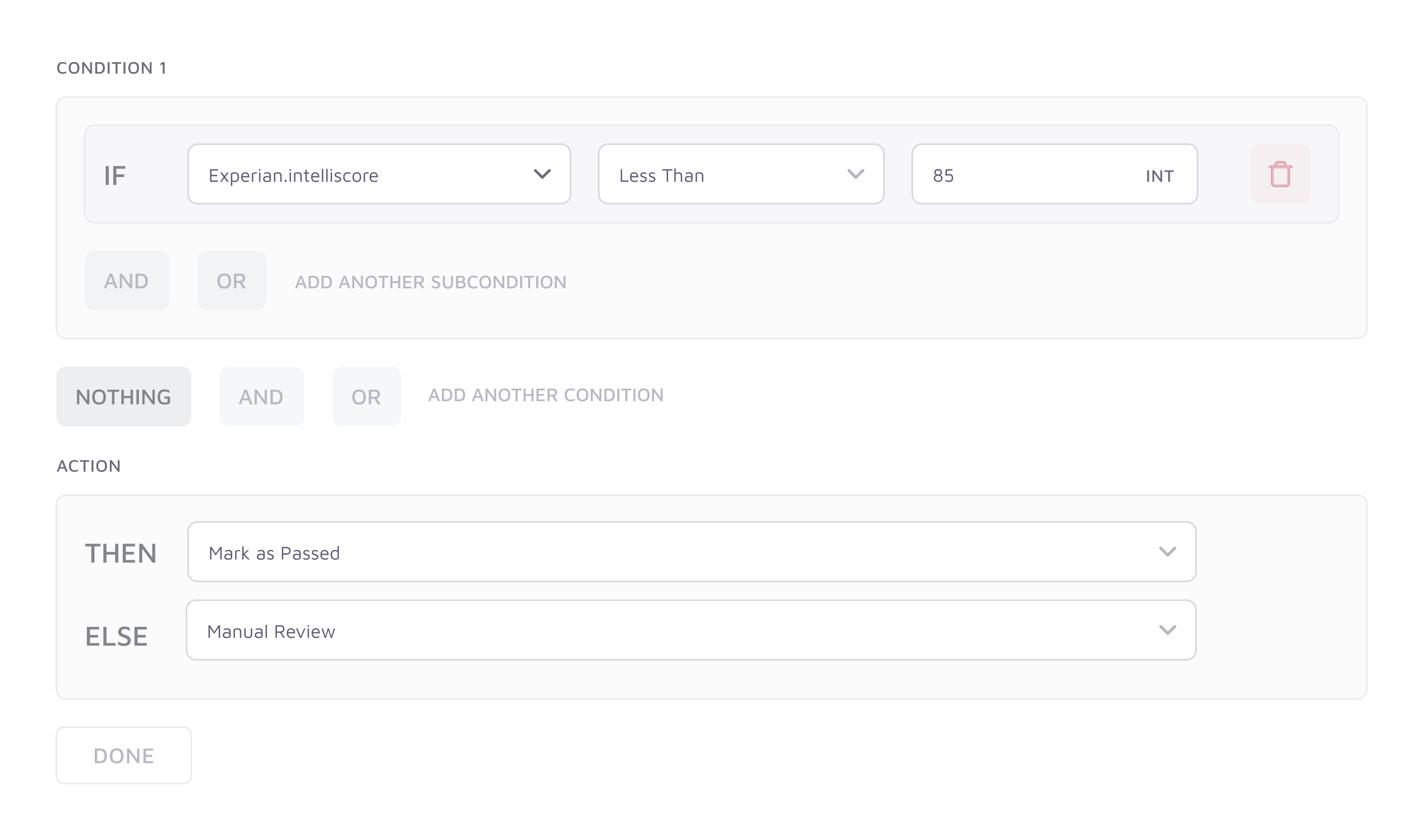

With Noble, firms can entry credit score bureaus, banks and revenue verification suppliers in deciding to which clients to increase credit score strains (e.g. loans and money advances). The platform’s interface lets companies deploy workflows that mechanically approve, decline or flag customers for guide evaluations, whereas on the backend customizing the expertise to match a model and auditing underwriting information from a single view.

“This will increase lifetime worth, boosts buyer retention and in the end could be a completely new income supply for firms,” Biger asserted. “Noble empowers … firms to do that rapidly and effectively with out expending a lot inside engineering or product sources.”

Daniel Aronovitz, principal at Perception Companions, sees Noble’s main clients as fintechs, software-as-a-service firms with monetary choices and B2B marketplaces and wholesalers. It’s early days, however he claims that the corporate already has “tens” of shoppers together with main fintechs, with “hundreds of thousands of {dollars}” of loans originated via the Noble platform.

“With its sturdy product choices and spectacular founding workforce, Noble has already acquired B2B and business-to-consumer clients throughout use instances,” Aronovitz stated in an emailed assertion. “Noble has created a platform for credit score underwriting infrastructure as a service, enabling any firm to construct proprietary credit score merchandise in-house.”

Conditional logic in Noble’s credit score decisioning engine. Picture Credit: Noble

However Noble isn’t distinctive in offering credit score infrastructure. Fintech startup Alloy, which final 12 months raised $100 million at a $1.35 billion valuation, not too long ago expanded into automated credit score underwriting. Stilt raised $114 million in March to develop its credit score choices. There are additionally corporations like Lastly, which concentrate on credit score merchandise for small- and medium-sized companies.

For his half, Biger believes the market is strong sufficient that Noble isn’t vulnerable to getting crowded out. He’s not essentially improper — credit score originated on the level of sale within the U.S. is projected to develop from about 7% of unsecured lending balances (i.e. with out collateral) in 2019 to about 13% to fifteen% of balances by 2023, according to a McKinsey report. By 2023, the report initiatives that “pay in 4” gamers — i.e. distributors like Klarna and Afterpay — will originate about $90 billion yearly and generate round $4 billion to $6 billion in revenues.

After all, credit score merchandise don’t assure income — the purchase now, pay later sector specifically has suffered steep losses and slashed valuations as of late. However Noble’s small-but-growing buyer base proves that some firms, not less than, are shopping for the gross sales pitch — and maybe seeing some success.

“There are just too many challenges that firms face when trying to construct credit score merchandise together with compliance, debt funding and underwriting,” Biger stated. “Noble’s mission is to take away these limitations and allow the inevitable motion of lending experiences from offline to on-line in the identical method that fee processing platforms constructed the brand new fee rails that enabled the explosive progress in on-line funds witnessed over the previous decade.”

Source link